Spanish Mortgage Floor Clauses

Floor Clauses Spanish Legal Reclaims

Spanish Banks Face Hefty Bill From European Court Ruling On Mortgage Index S P Global Market Intelligence

Amount To Be Claimed For The Suelo Floor Clause Mortgage In Spain

Floor Clauses Mortgage Reuters Solicitors

Mortgage Floor Minimum Interests Mortgage Clause Careful With The Bank S Agreement Lawyers

Is There A Floor Clause In Your Spanish Mortgage Agreement

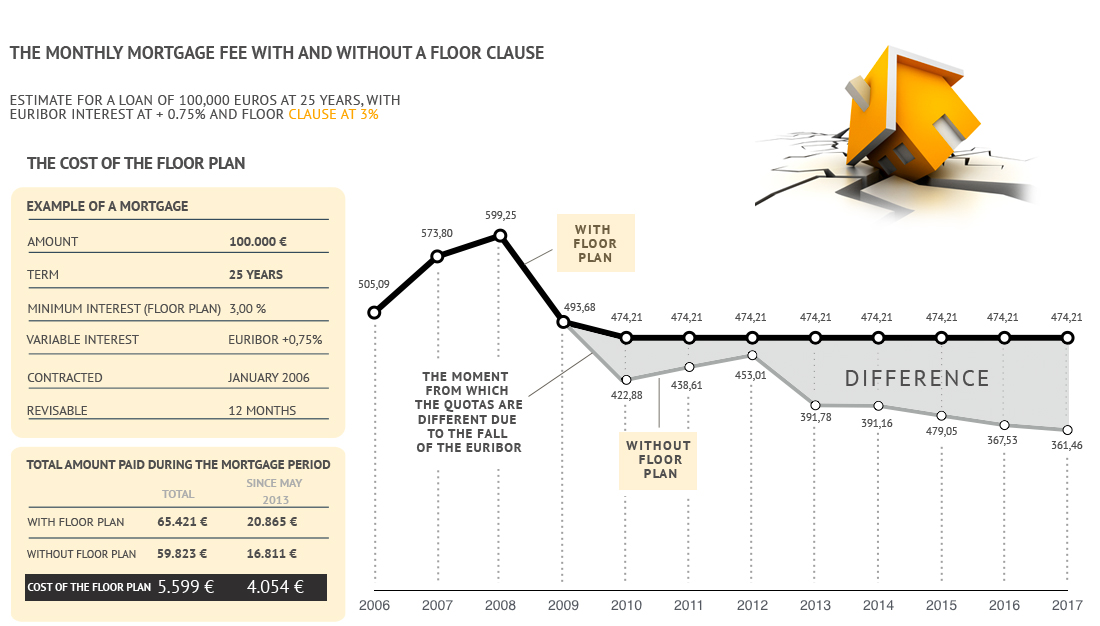

Floor clause basically in spain most mortgage loans are referred to the euribor rate plus a differential.

Spanish mortgage floor clauses. For most spanish mortgages the interest rate payable is calculated by reference to euribor or irph. The way that the floor clause was inserted into the mortgage agreement and how this was explained by the spanish bank to customers was not always clear or straightforward. Top 10 spanish mortgage abusive clauses. After the eu s ruling that the floor clause was abusive the spanish government set up a process to ensure that claims are dealt with swiftly.

Banks that simply removed the floor clause without taking any further action have also been sentenced to reimburse their clients. Clausula suelo floor clause 2. Free check spanish mortgage with floor clauses closer to a definitive solution for those affected the first thing i would like to do is inform you that c d solicitors has signed a collaboration agreement with the sevillian law firm gallego rivas which specialises in financial and banking law. A floor clause is the term used when the monthly interest on a mortgage does not go below a certain percentage if so then this clause could be considered to be abusive as a result of a spanish supreme court decision dated 9 may 2013.

Traditionally the borrower pays the set up costs for a spanish mortgage which amount to about 10 of the property s sales price and include registration fees notary fees and taxes. Irhp mortgage loan reference index 3. For most spanish variables rate mortgages the interest rate payable is calculated by reference rate to euro interbank offered rate euribor. A floor clause or clausulas suelo in spanish is simply a clause that has been inserted into mortgage agreements by some spanish banks that affects the interest rate payable on the mortgage.

The following list is not a closed one meaning i will only include the most common ones. A floor clause also known as clausula suelo or suelo hipotecario is simply a clause that has been inserted into variable rate mortgage agreements in spain during the last 20 years that affects the interest rate payable on the mortgage. Despite the clogged up spanish legal system causing delays for mortgage floor clause claims in 2017 taking your lender to court is still the most effective way to obtain a full refund on overpaid mortgage interest and the judicial authorities have announced measures to speed up claims in 2018. However patience is still necessary.

While the floor clauses chaos rages there are two further sources of potential windfalls for borrowers and pain for spanish banks. There are three types of claims on each mortgage. Mortgage fees valuation fee notary fee loan fee.

Crohn S Disease Crohns Crohns Disease Disease

New Spanish Mortgage Law 2019 The Spanish Connection

Mortgage Minimum Ground Or Floor Interest Rate Clauses Legal Claims

Should You Claim For Mortgage Floor Clause Or Arrangement Fee Expenses Money Saver Spain

Are You Eligible To Reclaim Overpayments On Your Spanish Mortgage Spain Property Guides

European Court Of Justice Slams Floor Clauses

Mortgage Floor Interest Abolished Take A Look At Your Interest Spanish Legal Services

Spanish Multi Currency Mortgage Claims

Spanish Bank Claims Mortgage Help Are You Due Compensation

Floor Clause Debacle Shows Importance Of Mortgage Brokers Agence Triton

What S Behind The Spike In Spanish Mortgage Activity Wsj

Carpetrunners12feetlong Small Spaces Desks For Small Spaces Small Space Hacks

Want To Know What Are Serviced Apartments How Serviced Apartments Can Be Your Home Away From Home Best Home Loans Best Mortgage Lenders